Back

Contents

Buy Side and Sell Side Liquidity – How Does It Work?

Technology

Iva Kalatozishvili

Business Development Manager

Demetris Makrides

Senior Business Development Manager

The concepts of buy and sell side liquidity play an important role in financial markets. Liquidity refers to the ease with which assets can be purchased or sold, and identifying areas of strong liquidity can provide valuable insights into market behaviour. This article will define the buy and sell sides, explain the concept of liquidity, and explore how liquidity works in practice.

The buy side encompasses institutional investors like hedge funds, pension funds, and asset managers who purchase securities. The sell side refers to brokers, banks and other firms involved in issuing and trading assets. Both sides interact to facilitate markets, with liquidity emerging from their aggregate activities. By understanding where liquidity accumulates, we can anticipate potential price moves and improve our trading.

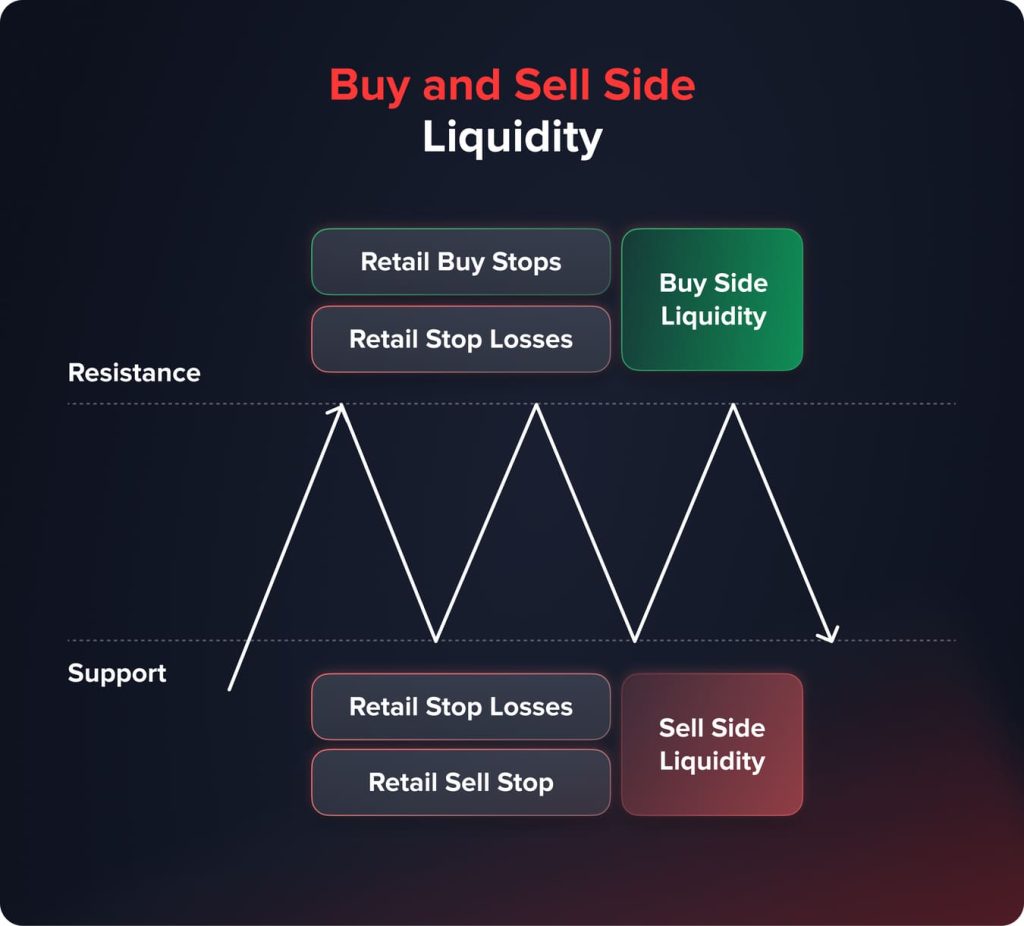

What is Buy Side Liquidity?

Buy side liquidity emerges from the positions of traders who have sold short. Understanding where these short sellers typically place their protective stop-loss orders provides valuable insight into potential buy side liquidity zones.

Buy side zones typically form above prominent resistance levels. Resistance is where an uptrend fails to continue climbing higher, marked by decreased buying enthusiasm and increased short-term positions taking place above that price level. For active assets, there is often clustering of short-term short positions that create visible buy side zones just above psychologically round numbers or technical price levels where prior selling was seen.

Traders will watch for important resistance levels to potentially attract short-term short sellers, such as whole numbers, moving averages, trendlines from peaks or troughs, and Fibonacci retracement levels useful for identifying possible short-term resistance turned potential buy side zones. Short sellers reasoning the upside momentum has expired may enter shorts at or above these technical levels.

For instance, if a stock runs into resistance at $50 and therefore entices short positions, the short sellers’ rationale for a pullback would have them place protective stop losses $1-2 above at $51-52 as their lowest acceptable exit price.

Now, if the selloff starts running out of steam and some buyers come to force, in trading and are able to push through this identified buy side zone of $51-52, the buying orders will start queuing up through and above $51-52 as stops are triggered, which in turn catalyzes lots of short covering, fueling the price ever higher.

In consolidating markets where support and resistance are redefined, buy side liquidity may get tested multiple times. As levels are retested, short sellers may carefully lift the location of higher stop orders on a pullback after a level is reproved. The clustered stopping zones above evolving resistance can be especially revealing of shorts if they are broken in a manner that sparks short-covering-driven accelerations higher.

What is Sell Side Liquidity?

Sell side liquidity zones emerge from the positions of traders who have established long positions within an asset. These are formed below key support price levels, where traders on the long side of the market will have an interest in defending any latent downside risk.

It forms support as it finds a price level at which it doesn’t want to push below and acts as the staging ground for further thrust upward. Traders try to figure out where a potential uptrend found a constructive base, such as whole numbers, moving averages, or recent lows trendline touches. And in such technical locations, longs will tend to congregate.

As security climbs from foundational support areas, emboldened bulls defend each subsequent higher low by strategically placing their protective sell stops below these successive support checkpoints. This clustering of long exit orders underneath evolving foundation levels carves out distinct sell side liquidity zones.

If selling unexpectedly resumes, piercing through a deeply fortified accumulate zone can spark a wave of long liquidation. As stops are triggered off in rapid succession below, the released supply dumps the price further downward at an accelerated clip.

In protracted downtrends, repeated tests of lows see additional sell side liquidity levels stack up successively lower as longs steadily raise their hedged stopping zones. More short-term selloffs are often precipitated by violations of these dense zones.

Sell side liquidity offers clues about potential pivot points by understanding how prevailing market participants have strategically hedged their risk. Its monitoring adds context for traders when seeking entry/exit spots around imminent support levels.

You may also like

Demetris Makrides

June 17, 2024

Differences Between Buy and Sell Side Liquidity

While buy side and sell side liquidity emerge from comparable mechanisms involving the strategic hedging of positions by market participants, there are some important distinctions between the two in terms of overarching goals, clientele served, core functions, compensation structures, and regulatory frameworks.

Goals

The buy side primarily focuses on outperforming over a more extended time horizon through superior investment selection and portfolio management. Its aim is profitability and asset under-management growth.

While the Sell side functions target the relatively different goal of enabling market transactions through a new offering of securities, liquidity, and research, which can be further described as revenue generation through fees, commission, and spread. They basically act as an agent between the issuer and the investor.

Clients

The buy side caters mainly to significant institutional investors, including pension funds, endowments, hedge funds and high-net-worth individuals. These clients are looking for an edge in terms of best risk-adjusted returns.

The sell side serves both the corporations issuing the securities, and all classes of investors from retail traders to larger financial institutions looking to transact. As a result, their client base is significantly more varied.

Functions

Functional activities of the buy side core involve in-house research analysis of securities and investment followed by direct deployment through portfolio management to create alpha. The sell side entails underwriting new issues, making markets, sales/trading, investment banking advisory work, and investment banking research distribution. Where issuers are connected to investors through a wide range of services in capital markets.

Compensation

Buy side compensation structures also tend to place more emphasis on performance-based bonuses that directly link pay to the investment outcomes achieved for clients. In comparison, those who work on the sell side generally earn fixed salaries but can also receive additional transaction- or commission-based compensation, which will depend on deal flow and the number or size of trades executed.

Regulations

Although both are controlled by the SEC and related state regulators, fiduciary responsibilities for the buy side go so far as advice. The strict legal boundaries aim at minimizing conflicts of interest in dealing with the customers’ funds. On the sell side, the regulation aims more at market integrity and transparency in being middlemen.

In summary, there are meaningful distinctions between the ultimate goals, functions and incentives driving behaviour on the buy versus sell sides of global financial markets. An appreciation of these differences goes a long way towards understanding liquidity dynamics.

You may also like

Demetris Makrides

June 4, 2024

Pros and Cons of Buy vs Sell Side Careers

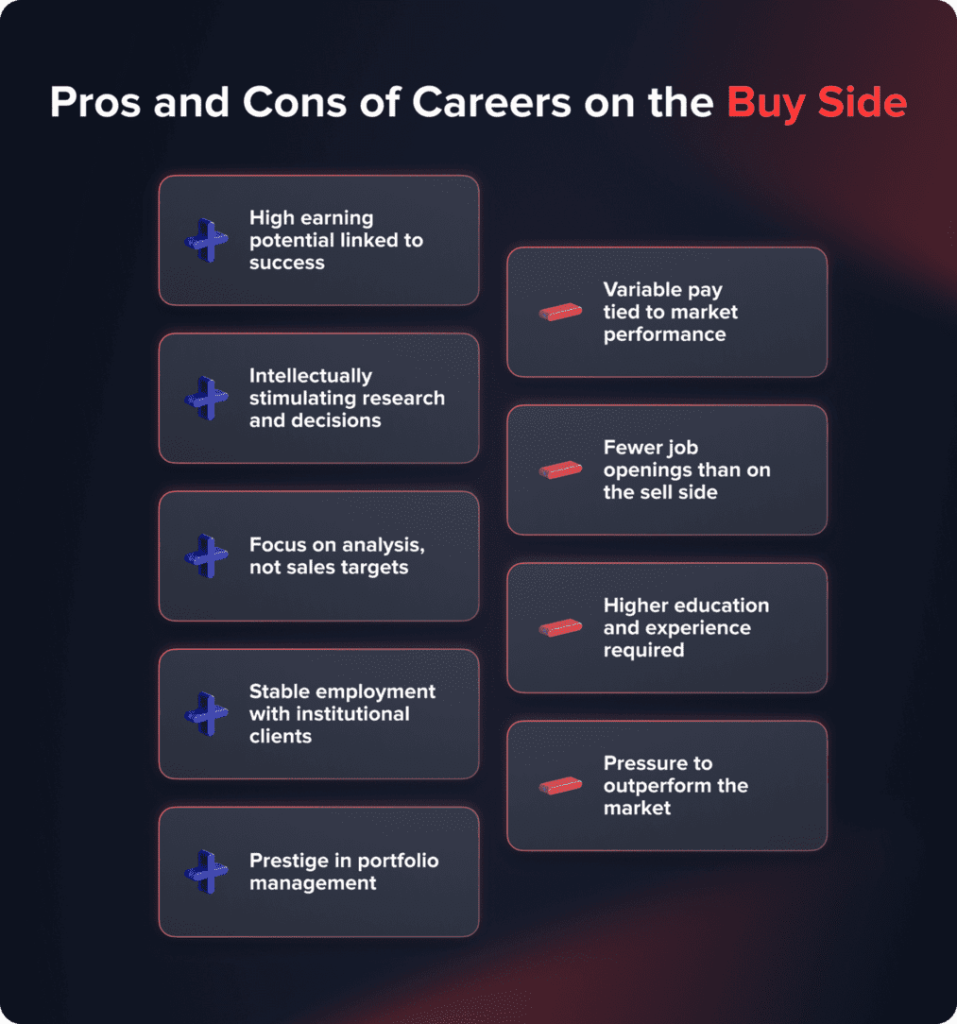

Pros and Cons of Careers on the Buy Side

Potential Pros

- Compensation structures directly link pay to investment performance outcomes via bonuses, offering the potential for higher earnings in successful years

- Intellectually stimulating nature of conducting independent research to identify overlooked opportunities

- The focus is on analyzing companies and making well-informed investment decisions rather than sales targets

- Typically more stable employment given clients are primarily large institutional investors

- Prestige associated with portfolio management roles at sizeable investment firms

Potential Cons

- Total compensation is variable year-to-year depending on market conditions and investment returns generated for clients

- Substantially fewer available positions relative to the sell side given the buy side represents a smaller segment of the overall financial industry

- Higher educational and experience prerequisites are generally required to gain access to coveted buy side analyst/portfolio manager roles

- Greater pressure to outperform market indexes and defend investment decisions/theses during difficult periods

Pros and Cons of Careers on the Sell Side

Potential Cons

- Far more entry-level jobs are available in sales, trading, investment banking, and research providing multiple options to break into the industry

- Excellent training grounds that develop real-world client interfacing skills highly transferable to other domains

- Fixed salary compensation still applies even during equity market downturns or deal droughts

- Career advancement attainable within comparatively larger organization structures

- Various practice areas allow flexibility to explore different career paths

Potential Cons

- Revenue generation obligations and individual production targets introduce stress around business generation

- Compensation consists primarily of base pay with bonuses geared towards transaction volume metrics rather than investment outcomes

- Longer hours are typically required in client-facing sales/banking roles supporting rigorous travel schedules

- Potential conflicts of interest may exist when recommendations meet corporate banking objectives

- Early exits are often required to transition onto more lucrative buy side opportunities

Overall, both the buy side and sell side offer fulfilling long-term careers in finance, each with its advantages and trade-offs to consider carefully depending on individual interests, skills, and lifestyle preferences. With experience, both paths can establish a strong professional foundation.

How To Identify Liquidity Zones

Technical tools can help to identify liquidity zones. More often than not, Fibonacci retracement and extension levels identify the buy and sell side areas nearby that can equate to proportionate movements. Zones regularly see convergence with simple moving averages weighted for different periods. Horizontal and trend line analysis also indicates boundaries where the momentum was stalling before.

Breakout and reversal candlestick patterns provide visual clues about ongoing battles between bulls and bears near prominent liquidity territories. Formation types such as spinning tops or downs signal heightened indecision while engulfing bars flag decisive moves breaking thresholds.

There is a layered form of history in volume profile indicators, which graphically display price levels that differentiate where the bulk of trading activity has occurred—thus identifying key supply and demand centres in the market. Formations of spikes validate the intensification as the zones are disintegrated under pressure. The point of control pinpoints the most traded price.

Real market examples prove instructive. One stock declined to support under $15 and consolidated sideways for weeks within a $13.50 sell side zone where buying repeatedly absorbed downside tests. Heavy turnover marked this level as a substantial supply. Its puncture catalyzed a surprising two-dollar plunge lower as hopeful short-term bulls bailed en masse, with stops triggered in tow below.

Monitoring confirmed liquidity zones offer actionable insight into potential support/resistance flips. Case studies apply this framework demonstrating identifiable behaviors traders can integrate. Ongoing observation strengthens pattern recognition when seeking opportune times to trade evolving market structures.

How To Trade with Liquidity in Mind

Finding liquidity zones sets the stage for planning strategic manoeuvring. When the accumulation and distribution territories take form, the traders can position themselves relative to those concentrations. Doing so provides potential pivots to regain or protect exposures.

Breaking above buy side resistance or below sell side support often sets up an extension that is not sustainable. Selling into runs or going short targets the next stacked zone once momentum stalls. Weak, delayed breakdowns through the sell side areas create a gap that traditional traders target to buy. The aggressive long entries chasing holds above these lower-value pockets.

Zones invite periodic retests, keeping the implied volatility elevated. Selling out-of-the-money puts collects income as zones prove resilient. Stops respecting untested adjacent zones balance rewarding trends with minimizing the drawdowns if reversed. Trailing breaks improve risk-defined holds.

Upside purchase constraints use higher-level expansion in time frames, with downside profit objectives pointing to the proximity of underlying support. Integrating structure given through supply and demand areas, either buying with, against, or in the absence of the prevailing sentiment, improves trade construction.

The perceptions of those zones remain in tune with the changing market conditions and the shifting behaviour of participants since the updating is constant. Keeping an eye on changing liquidity maximizes opportunity around confirmed zones. The framework is useful for assessing what the potential risk/reward could be between the fluctuations within the cycles.

Tips For Monitoring Liquidity Levels

For a trader, it’s still important to monitor changes in liquidity and market structures through time. Groups inclined to one side will consolidate in the range, all the while narrowing on which sides are building conviction, while breakouts will reveal which bias took control. Diminishing conviction in a direction is what will be shown if the bands of volume are receding, while for the opposite, expanding bands are shown.

Charting liquidity patterns daily is a very valuable context during emerging moves. An update makes it easy not to hang onto the outdated perceptions that offend the language of the market for that day. Liquidity not only evolves over the course of days but it changes during the day, as different groups of participants come into and out of the market.

Phases of auction into the open will shape the prevailing structure for the near term. Later then into the close, selling exhaustion often results in range contraction. Knowing how these factors impact the day will help in the timing of entries in terms of the prevailing conditions.

In trending states, liquidity gradually flows deeper in the prevailing direction as zones stack closely along, following the momentum. Consolidating markets see this liquidity flip-flop between defined levels. Here, traders engage in a debate as to which side the range might eventually find a resolution to and the force set for a reevaluation.

The major news can trigger sharp moves as the market resumes an established trend or if the range eventually breaks out of indecision. In quiet periods with no big news or events, the ranges widen in a free test of wills on both sides. Measuring the broader macroeconomic variables and changes in policy will keep expectations for the potential for stability or volatility on the ground.

Monitoring liquidity levels closely will enable an outline of the market structure to be laid out, including shifts in sentiment and potential turning points for trade selection. It helps us steer through the various phases of a broad cycle.

Conclusion

Defining buy and sell side liquidity levels advantages traders. Locating major order flow zones informs potential support/resistance flips fueling reversals. Monitoring changing structures empowers adapting strategy according to market mood and participant behaviour. While not predictive, integrating liquidity awareness improves understanding of mechanics driving prices across cycles.

12 March, 2025

NEW POST FOR TESTING BLOG AND WP

What is Lorem Ipsum? test link with http Lorem Ipsum is simply dummy text of the printing and typesetting industry. Lorem Ipsum has been the industry’s standard dummy text ever since the 1500s, when an unknown printer took a galley of type and scrambled it to make a type specimen book. It has survived not only […]