Volver

Contents

What Is Asset Allocation and Why Is It Important?

Business

Iva Kalatozishvili

Business Development Manager

Demetris Makrides

Senior Business Development Manager

Asset allocation refers to how investors divide their funding portfolio among exclusive asset classes based on their financial dreams, threat tolerance, and time horizon.

By investing across various assets, investors can balance risks and rewards to maximize capability returns. This method of diversification forms the muse of wise funding management.

This article will uncover asset allocation, how investors can decide their top-of-the-line allocation and techniques for implementation and monitoring allocations over time. We will study problems like how financial conditions can impact allocation selections and commonplace mentally demanding situations traders may additionally face. The motive is to explain why asset allocation is such a crucial idea for both newbies and experienced investors alike to correctly manipulate their tough-earned financial savings.

With a balanced approach tailor-made to at least one’s situation, asset allocation can assist people in obtaining their monetary desires with the suitable stage of risk. By studying on, you may benefit from a thorough knowledge of this important funding exercise and approaches to incorporate it into your portfolio for long-term success in the markets.

What is Asset Allocation?

Asset allocation is the process of dividing an investment portfolio among different financial assets, such as stocks, bonds, and cash equivalents, with the goal of optimizing the risk and potential returns based on the investor’s risk tolerance and investment horizon. More specifically, asset allocation refers to how an investor divides up their portfolio across major asset classes. The three main asset classes are stocks (equities), bonds (fixed income), and cash/cash equivalents.

By investing across different asset classes, investors can aim to reduce portfolio risk through diversification, as assets don’t always move in the same direction. For example, when stocks decline, bonds may hold their value or increase. The appropriate asset allocation mix for each investor depends on their risk tolerance (what level of volatility they’re comfortable with) and time horizon (how long they have until needing to access the funds).

A strategic asset allocation takes into account these factors to determine the optimal percentage invested in stocks, bonds and cash to maximize returns for each level of risk. Asset allocation is an important portfolio management strategy because it allows investors to take as much or as little risk as fits their financial situation and goals. Proper diversification through asset allocation aims to balance risk and potential returns.

So in summary, asset allocation is the process of distributing an investment portfolio among major asset classes to reduce risk and optimize returns based on personal investment profile and objectives. It is a core principle of building well-rounded, balanced investment portfolios.

The Main Asset Classes

The three main categories of all investment options are stocks, bonds, and cash equivalents. Let’s examine each more deeply:

- Stocks (Equities): Ownership shares in public companies that have provided the highest returns over the long term but also experience frequent short-term volatility in their prices.

- Bonds: Essentially loans made to entities and governments, offering interest payments to bondholders but with principal values fluctuating as interest rates change. Bonds tend to be less risky than stocks.

- Cash Equivalents: Highly liquid assets like savings accounts, and money market funds that aim to preserve your principal through very low returns. Considered the most conservative option.

Within these broad asset classes exist numerous sub-categories providing different risk-return profiles. Some examples include large cap versus small cap stocks which refer to company size, domestic versus international equities, and investment grade versus junk corporate bonds that vary in credit quality. There are also government bonds of different durations from short to long-term and index mutual funds versus actively managed funds.

You may also like

Vitaly Makarenko

June 26, 2024

A core principle in asset allocation is that high returns require higher risk. History has proven this risk-return trade-off between asset classes, as stocks have outpaced other assets significantly over the decades yet come with sharp downturns periodically. Bonds and cash, though less volatile, have netted more modest long-haul gains. By diversifying across these varied investment types, individuals can optimize their portfolios for maximum returns within their accepted risk tolerance.

Core Concepts in Asset Allocation

Three important concepts help guide your asset mix decision-making:

- Risk Tolerance: How much volatility you are psychologically comfortable enduring

- Time Horizon: When you anticipate requiring access to invested funds

- Diversification: Holding a variety of assets whose risks offset each other to various extents

By understanding these factors, you can optimize your portfolio for maximum returns with an acceptable level of risk exposure based on individual goals, timelines, and tolerance for short-term market fluctuations.

Determining Your Asset Allocation

Crafting an optimal asset mix involves analyzing a variety of specific personal factors. By closely examining each influential element, investors can design a customized allocation in line with goals and temperament. Several critical aspects shape appropriate risk tolerance and asset weights:

- Age: Younger investors have decades until major life events allowing flexibility to assume risk in early career years seeking growth. Those nearing retirement prioritize capital preservation as time diminishes for losses to subside.

- Financial Objectives: Goals like saving for a home purchase within 5 years necessitate a different allocation than growing a nest egg over 40 years for a comfortable post-career lifestyle. The further off the objective, the more aggressive the allocation can be when aiming to maximize returns over an extended period.

- Risk Tolerance: Individual capacity for withstanding short-term volatility while maintaining a long-term perspective differs depending on personality, existing assets, and ability to recover from potential downturns. Tolerance informs appropriate equity exposure.

Common Allocation Guidelines

A frequently cited rule uses age to estimate equity exposure. The approach suggests subtracting your age from 110 to determine your stock allocation percentage. For example, at 40 years old, the formula would indicate holding your portfolio at 70% stocks (110 – 40 = 70). However, simplistic models seldom address complex personal realities.

More instructive reference points are hypothetical model portfolios displaying conservative, balanced, and aggressive strategies. Conservative mixes (20-40% equities) emphasize risk management over returns. Moderate blends (40-60% equities) balance the two priorities. Aggressive allocations (60-80% equities) focus on long-term growth through maximum stock exposure.

Comparing one’s tolerance and timeline to various sample portfolios serves as a useful starting point. But individualization is key, as no two financial situations are alike. Distinct health, dependents, income variability, career risks, and more warrant custom consideration.

Experienced advisors can structure bespoke allocations accounting for nuanced needs and comfort levels. Rather than relying on formulas alone, factoring unique career phases, dependents, job security, and likelihood of future earnings or inheritances leads to allocations tailored for each. Personalized planning ensures appropriate risk-taking to destination goals through changing conditions.

Implementing and Maintaining Your Asset Allocation

Once an appropriate asset mix is determined, the next critical step is selecting tools to execute the plan efficiently over time. Several low-cost options exist:

- Broad market index funds provide diversified exposure at minimal cost by passively tracking segments like domestic/international stocks and bonds. This allows for covering all bases affordably.

- ETFs (exchange-traded funds) offer a similar ability to construct globally diversified, cost-efficient portfolios targeting specific factors through numerous precise investment vehicles.

- Target-date funds automatically rebalance a pre-set, risk-adjusted portfolio increasingly conservative as the target retirement year nears. This provides simple, hands-off management aligned with one’s timeline.

- Robo-advisors construct customized, digitally managed portfolios based on an investor’s risk profile and goals, maintaining ongoing oversight at low fees relative to traditional advisors.

Regardless of the implementation of the vehicle, routine maintenance is vital. Natural market fluctuations inevitably alter percentages over the years, necessitating periodic rebalancing transactions to restore intended risk level allocations. Unchecked drift could undermine strategic objectives.

You may also like

Vitaly Makarenko

May 1, 2024

Additionally, material life changes require ongoing review and potential adjustment. Events triggering new analysis may include marriage, children, job loss, inheritance, or evolving priorities. Ensuring portfolios evolve alongside changing needs optimizes chances of achieving dynamic personal objectives. Regular oversight maintains dynamic strategic logic as situations transition through life.

Combined, systematic implementation and conscientious maintenance create the foundation necessary to fulfil asset allocation’s fundamental role as a long-term wealth-building framework aligned with each unique financial identity.

Economic and Market Impacts on Asset Allocation

Perhaps the greatest influencers of strategic asset allocation are the prevailing economic climate and the performance of financial markets. Prudent investors must thoughtfully respond to these changes over time. During periods of economic expansion and bull equity markets, stocks often outpace other assets as corporate earnings rise steadily. Consequently, growth-oriented portfolios are dominated by equities aligned with expansionary conditions.

However, economic contractions and recessions typically coincide with declining stock prices in the near term as uncertainty increases. At such times, a more conservative stance focused on fixed income and cash better preserves capital by avoiding downturns. Interest rate environments also necessitate a nimble response. Rising rates cause bond prices to drop, favouring shorter-term debt or equities. Conversely, inflationary patches increase the appeal of inflation-linked bonds, commodities, and real estate offering inflation protection.

Rather than set-and-forget portfolios, regularly evaluating macroeconomic and capital market signals indicates when to shift allocations between offence, defence, or quality-focused positions. Re-profiling for prevailing conditions optimizes risk-adjusted returns through varying cycles. Close monitoring of these potent demand-side factors prevents stale, static strategies from disregarding changing fundamentals. A dynamic approach that systematically responds to shifts remains prudent as situations evolve over business and credit market fluctuations.

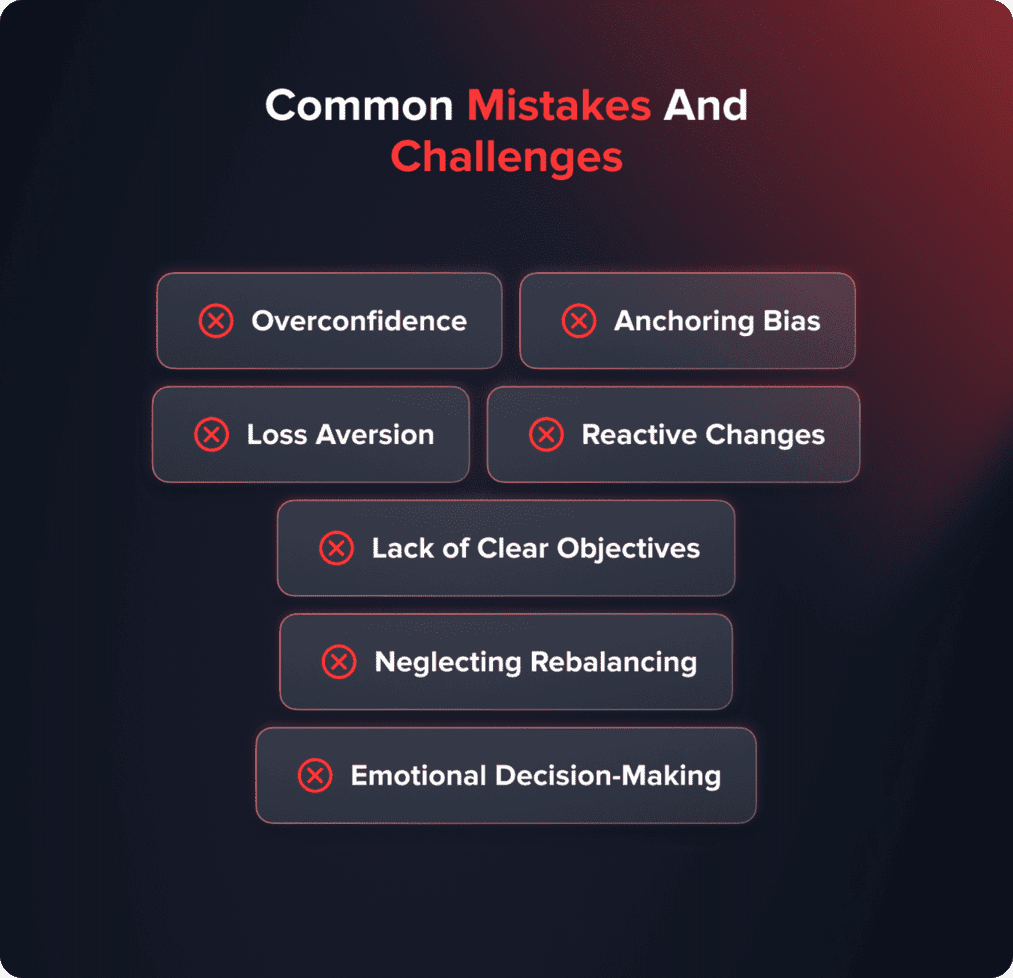

Common Mistakes and Challenges

While asset allocation provides a rational framework, innate psychological tendencies can undermine even the most carefully crafted plans if left unrecognized. Self-awareness of these biases is key to long-term success.

- Overconfidence leads to recency bias, assuming that recent conditions will persist instead of reversion to long-term norms. This causes many to chase momentum at market highs.

- Anchoring bias skews decisions based on early results rather than considering all available information objectively.

- Loss aversion creates paralysis during downturns precisely when reinvesting would prove most beneficial. Just as emotions intensify in difficult times, cognitive biases emerge strongest.

- Reactive changes centred on short-term noise rather than personal circumstances frustrate true risk management. Only post-correction adjustments come too late.

- Clearly defining objectives and risk appetite upfront provides accountability during inevitable volatility.

- Automating periodic rebalancing overrides impending excitement or distress, adhering to a long-term view.

- Conscientious review counters the tendency to make imprudent decisions when volatility peaks emotionally.

By understanding typical heuristical errors, an investor can circumvent wealth erosion through a commitment to disciplined allocation maintenance aligned with their intended strategy rather than fleeting sentiments. Self-awareness paves the path to long-term success.

Bottom Line

Asset allocation provides a foundational approach to investing by diversifying across complementary risk and return profiles suited to individual goals, risk capacity, and investment horizons. When thoughtfully designed through careful consideration of a multitude of personal factors and flexibility to adapt to changing needs and environments over time, strategic diversification allows maximizing returns per unit of risk accepted.

However, ongoing maintenance including periodic review and rebalancing is crucial, as is an unbiased, rationale-based perspective, to overcome behavioural biases that could undermine the framework’s ability to effectively accomplish its vital role in long-term wealth accumulation tailored to each unique situation.

12 de marzo de 2025

ES VERSION OF NEW POST FOR TESTING BLOG AND WP

What is Lorem Ipsum? Lorem Ipsum is simply dummy text of the printing and typesetting industry. Lorem Ipsum has been the industry’s standard dummy text ever since the 1500s, when an unknown printer took a galley of type and scrambled it to make a type specimen book. It has survived not only five centuries, but also […]